In a world of do-it-yourself home improvement programs and YouTube repair videos, it can be tempting to manage your own money. So, why might one consider working with a professional? And how should you think about the costs and benefits when selecting a professional to work with? Here’s what individual investors should know when assessing the value of working with a financial advisor.

Why Partner with a Financial Advisor?

A financial planner can create a comprehensive, tax-efficient wealth strategy based on your goals, risk tolerance and current financial situation. Knowing you have a trusted professional helping to navigate your needs and make informed decisions also brings peace of mind.

While there are many ways to weigh the benefits of working with an advisor, one way is to explore the main costs you might face in your financial planning journey.

- Economic costs: There is an opportunity cost for choosing one investment over another. How do you know which one is right for you, for your plan and for your family? Which one will give you the greatest likelihood of achieving your financial goals?

- Tax cost: Depending on which investments you choose, there are tax costs based on the titling of the asset, the investment type, the account type and the time when you buy and sell. How do you measure the time spent navigating the different tax treatments and consequences for your investments?

- Emotional cost: What are the trade-offs between managing your priorities, and are there strategies to reduce emotional costs? What is that worth and how do you begin to quantify it?

Along your journey, an advisor can help you assess these decisions and build a financial plan that aims to address your biggest needs, as well as uncovering those you may not have considered before.

An Advisor’s Advice Should Be Unique to You

Participating in an exploratory meeting specific to your needs, wants and wishes is the best way to identify if a relationship with an advisor may be beneficial and if there is value. It’s important to get a sense of the advisor’s standard of care, level of detail in their planning, how much they value building a relationship, and how they will coach you on financial behavioral decisions. When valuing an advisor, it’s best not to compare our experience with those of others. Although the relationships our parents or friends have with their advisors can shape our impression and outlook on the industry, what may be important to them and what drives their decisions may not be the same for us. Make sure your advisor is building a plan designed specifically for your needs and goals.

Assessing the Value for the Advisor’s Services

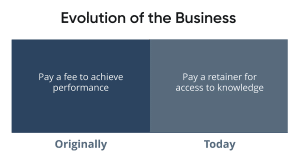

As we think about how to measure the value of an advisor, it is important to understand the evolution of the financial advice industry. The industry started as a way for wealthy individuals to gain access to financial markets. In fact, in the early 1970s, the top 1% of earners in the U.S. held over 50% of all outstanding stock. At that time, individuals looking to make an investment in a listed security, such as a stock or bond, could only do so through stockbrokers who would earn a commission for executing the buying and selling of a listed security. Thus, individuals were optimistically paying for high investment performance as brokers would buy securities in the hope of appreciation that would also serve their own needs via commissions. Very rarely would an individual buy a security solely because of how it fits into their larger plan. This is how the financial advice industry has evolved today, as the fee-based industry began taking off.

The Transition to a Fee-Based Industry

The rise of the internet in the early 2000s paved the way for disruptors to enter the financial services market, giving the public greater access to information on pricing and investments. This drove down what were once tremendously high trading fees. Discount brokers such as online trading platforms emerged, making it easier for investors with less money to make trades. Today, with discount brokerage firms offering broader access to financial markets, trading fees are zero in some cases.

However, these services do not offer the investment selection guidance that stockbrokers offered. That’s where the present-day, fee-based advisor enters the picture. Although there are several models for paying for financial advice, charging a fee based on assets under management has become one of the most common.

The Future of Paying for Financial Advice

We believe that paying a retainer to ensure you are on the right trajectory and for access to knowledge and advice that is specific to you and your circumstances is the future of the financial advice industry. It is not just paying for the answer to a specific problem but paying for the advice for unknown problems that only come through working with an objective, third-party advisor that has the professional competency, stays current, pays attention and creates the confidence that working with them will create the future you want. Schedule a Consult

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accurcy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. Buckingham is not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this article.

Buckingham Strategic Partners

When advisors work with Buckingham Strategic Partners, they gain the strength of a nationwide community of wealth management professionals. With the support of a diverse team of financial planning leaders, tax professionals, investment researchers and portfolio managers, advisors are able to orchestrate a bespoke plan, tailored to each client’s unique situation. Clients benefit from Buckingham’s team of dedicated professionals who are constantly exploring and assessing the ever-changing landscape of investments, tax code, markets and planning strategies—with a singular focus on maintaining an evidence-driven, fiduciary approach that puts client’s interests first.